FREQUENTLY ASKED QUESTIONS

You’ve got questions? We’ve got answers.

We get it… all this industry jargon can be exhausting and confusing, even to the most seasoned real estate investors. Let us help by explaining everything in plain English. You can consider us your new buddies who happen to be experts in finding the best funding solutions for short-term rentals and other real estate investments.

GENERAL FAQs

-

No, Host Financial can only lend on non-owner occupied homes. Primary homes and secondary vacation homes for personal use do not qualify.

-

A Debt Service Coverage Ratio (DSCR) loan is a type of real estate loan where the lender underwrites and approves the loan on the property's cash flow and its ability to cover the mortgage payments (principal and interest, property taxes, insurance and HOA fees) rather than primarily focusing on the borrower's personal income via W2's, Tax Returns or personal Debt to Income Ratio.

-

DSCR is calculated by dividing the property’s gross annual income by its annual mortgage debt service (including principal and interest, property taxes, insurance and HOA fees). A DSCR ratio of over 1 means the property generates enough income to cover its debt obligations. Host Financial can finance deals with DSCRs .75 or below. 75 to .99, 1.00+, 1.25+ and above. In the rate calculation DSCR ratio plays a factor so for the best rates not withstanding of other qualifying factors (FICO, loan size, property type, LTV, etc), a DSCR ratio of 1.25 above would be considered a top tier bracket for rates.

-

DSCR loans are commonly used by real estate investors, particularly those investing in rental properties, as these loans focus on the income-generating ability of the property rather than the borrower's personal finances.

-

DSCR loans can be used for a variety of properties, including single-family homes, condos, multi-family properties, and mixed-use properties.

-

The main benefits include less emphasis on personal income for loan approval, potentially faster approval processes, and the ability to finance investment properties based on their rental income potential. In addition you can vest a property under an entity such as an LLC instead of your personal name. This allows an investor to tie the debt to an EIN number rather than a Social Security Number, thus not reportable to personal credit score and affecting an investors debt to income score or negatively affecing their credit score.

-

The downsides might include higher interest rates compared to traditional loans, larger down payments, and the requirement of having a property that generates sufficient rental income.

-

A good DSCR ratio typically is 1.25 or higher. This ratio indicates that the property generates enough income to comfortably cover the debt payments with some margin.

-

Yes, it's possible. Since DSCR loans focus more on the property’s income potential, borrowers with lower personal credit scores might still qualify, although terms might not be as favorable. Best rates and LTV options exist at the 680+ credit bracket with top rate breaks occurring at the 760+ and 780+ credit brackets for most of our loan programs. 620+ credit score are financeable at higher rates and lower LTV options.

-

Refinancing a DSCR loan works similarly to other loans but will primarily focus on the property’s current income and its ability to service the new loan. If there property has 12+ months of historical income that can be used to underwrite the loan, if the property is a delayed purchase or fresh out of renovation, projected short term rental or long term rental income can be used depending on the intended strategy of the property.

-

Required documents typically include property lease agreements (if a long term rental), rent rolls, a schedule of real estate owned, property management agreements, and financial statements showing operating income and expenses. You can find more information on documents required for underwriting here.

-

Yes, DSCR loans are often used for purchasing new investment properties. Host Financial will evaluate the potential income of the property to determine loan eligibility.

-

Seasoning of rents refers to how long a property has been generating rental income. A longer seasoning can positively impact a DSCR loan application, as it demonstrates a history of consistent income generation.

-

Absolutely. DSCR loans are typically used for non-owner occupied properties, as the loan decision is based on the income produced by the property, not the owner's residence status.

-

Lenders take vacancy rates into account when calculating NOI for DSCR loans. A high vacancy rate may lower the NOI and, consequently, the DSCR, potentially affecting loan approval or terms.

-

Yes, borrowers can have multiple DSCR loans. These loans are often used by investors to build a portfolio of rental properties. However, each loan will be individually assessed based on the respective property's income.

-

All of Host Financials' DSCR loans require a personal gaurantee to be signed.

-

Renovations that increase a property's rental income can positively affect a DSCR loan by improving the property’s NOI and thus it's DSCR.

-

If the property’s income decreases significantly, it might affect the borrower's ability to meet loan obligations. In extreme cases, this could lead to loan default or the need for restructuring the loan terms.

-

Generally, yes, however rural properties can under scrutiny if running on a well and septic tank instead of city sewage. If a property is deemed too rural LTV restrictions may occur. Large acreages also play a factor in financing rural properties. Exception can be made on LTVs for rural properties on a case by case basis. Inquire with your Account Executive if the rural nature or large acreage of a property is a concern.

-

Interest rates on DSCR loans are generally higher than those on traditional mortgages due to the perceived higher risk associated with basing the loan on property income rather than the borrower's personal income.

-

No, currently financial only lends in the United States.

-

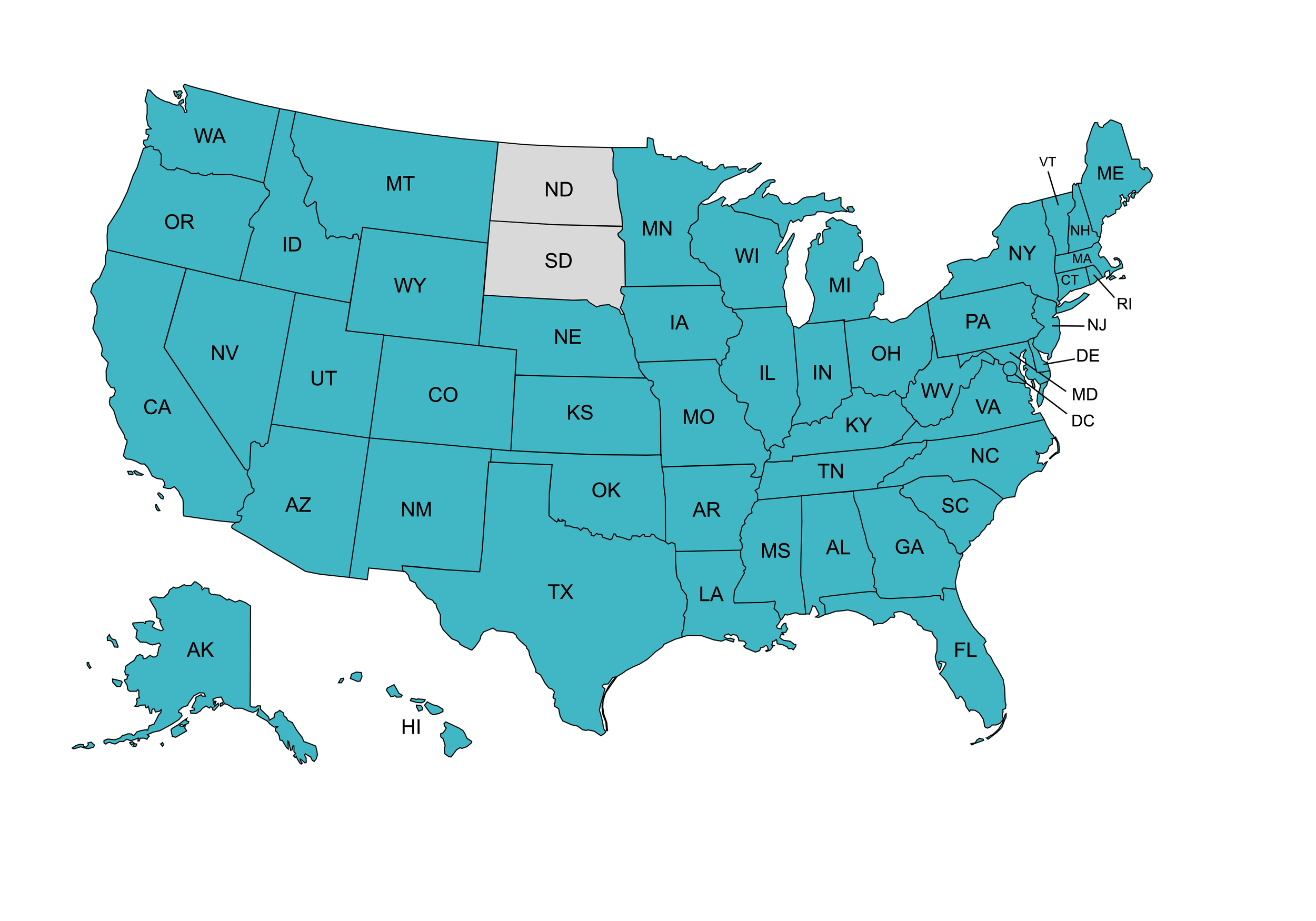

Host Financial lends in 48 states except North Dakota and South Dakota. See complete list below:

Alabama

Alaska

Arizona

Arkansas

California

Colorado

Connecticut

Delaware

Florida

Georgia

Hawaii

Idaho

Illinois

Indiana

Iowa

Kansas

Kentucky

Louisiana

Maine

Maryland

Massachusetts

Michigan

Minnesota

Mississippi

Missouri

Montana

Nebraska

Nevada

New Hampshire

New Jersey

New Mexico

New York

Ohio

Oklahoma

Oregon

Pennsylvania

Rhode Island

South Carolina

South Dakota

Tennessee

Texas

Utah

Vermont

Virginia

Washington

West Virginia

Wisconsin

Wyoming

STR LOAN FAQs

-

DSCR is calculated by dividing the property’s actual or projected gross annual income by its annual mortgage debt service (including principal and interest, property taxes, insurance and HOA fees).

Projected income can come from sources like AirDNA.co and Rabbu.com. For some programs the projected income is discounted by 20% for new investors and 100% can be used for experienced investors with 1 short term rental property owned within 100 miles of the subject property or a total of 3 short term rental properties owned nationwide.

If using existing income from a previous owner or a borrower owned property that is being refinanced, we can use 100% of the trailing twelve months of gross revenue or 100% gross revenue minus actual property management expenses in some cases.

A DSCR ratio of over 1 means the property generates enough income to cover its debt obligations. Host Financial can finance deals with DSCRs .75 or below. 75 to .99, 1.00+, 1.25+ and above. In the rate calculation DSCR ratio plays a factor so for the best rates not withstanding of other qualifying factors (FICO, loan size, property type, LTV, etc), a DSCR ratio of 1.25 above would be considered a top tier bracket for rates.

-

Host Financial provides financing for various properties suitable for short-term rentals, including single family residences, condos, townhomes, duplexes, triplexes, quadplexes, and multi-family properties up to 20 units.

-

Host Financial typically requires a minimum credit score of 620 for short-term rental financing. However, for the best LTV, rate, and term options a credit score of 680+ is preferred.

-

The approval process at Host Financial involves submitting a request for a quote, selecting the loan term and option to move forward with, proceeding with an application, providing documents for under writing such as entity docs (if vesting under an entity), driver's license, 2 months bank statements for liquidity verification, insurance policy quote, title report, and payment for appraisal inspection. Once borrower files, insurance policy, title reports, and appraisal report is submitted the loan will go into final underwriting and qualify control. Once approved, we prioritize a swift and efficient closing process that takes five to ten business days.

-

Host Financial offers flexible loan terms tailored to the unique needs of short-term rental investors. Choose from 30 and 40 year amortization options with 5/6arm, 7/6 arm, 10/6 arm, 10 year IO, and 30 year fixed options.

-

Yes, a down payment is required. The amount may vary based on factors such as credit score, property type, and loan amount. Host Financials' team collaborates with you to determine the most favorable terms for your specific situation. Typical down payments range from 15 to 25% down.

-

No, once Host Financial finances the property, you have the freedom to use it for short-term rentals as planned. However, it's important to consider and comply with local zoning and homeowner association regulations.

-

Absolutely. Host Financial takes into account projected rental income when evaluating your loan application from our partners at AirDNA.co and Rabbu.com.

-

Host Financial offers short-term rental financing with prepayment penalties ranging from 1 year to 5 years. Structures include option from a 5% or 3% flat prepayment penalty each year for the lenght of the pre-payment period term or a declining structure such as a 5/4/3/2/1, 5/4/2, 3/21, 3/0/0 (examples, not all inclusive).

-

Host Financial is committed to a smooth and timely closing process. While timeframes may vary, we strive to close short-term rental loans efficiently, typically within 25 days. The main timeframe hurdles for closing a loan that are outside of the borrowers control is the turnaround time on appraisal reports. In a cases in which insurance, title, appraisal report, and borrower side documents are turned in quickly closing can occur within one to two weeks from then.

-

• Host Financial Gets STRs: Host Financial can qualify loans using STR income projections from AirDNA and Rabbu or use existing STR income history, not just market rents like most DSCR lenders that claim they can do STRs.

• One Stop Shop For DSCR Financing: In our current dynamic market environment, rates and even qualification guidelines change daily. Host has access to multiple capital partners and will price the entire market ensuring you get the best rates and terms available.

• Should rates changes mid process we can quickly switch capital partners to get a lower rate.

• Should guidelines change mid process you won’t be stuck with a lender that has one set of guidelines which could kill your deal and put you back to shopping the market. This ensures we have the highest chance of closing on deals where others can’t.

• Host Financial are the experts in STR financing: 95% of our deals are for Short Term Rental Investment Properties. Working with Host ensures you know you’re working with a lender that gets it and can get the deal done. We’ve seen and done it all.

• Comprehensive Income Assessment: Host prioritizes finding the most advantageous financing options for your investment, which for DSCR Loans means looking at all potential property income numbers: Market Rents, STR Income History, or STR Income projections to see what qualifies you for the best rates and terms.

• Privacy & Asset Protection: With the ability to vest in an entity you can protect your identity and assets from the risks and liability involved with running a short term rental.

• Most coverage: Host lends in 48 states nationwide.

LONG TERM RENTAL LOAN FAQs

-

DSCR is calculated by dividing the property’s actual or projected gross annual income by its annual mortgage debt service (including principal and interest, property taxes, insurance and HOA fees). If the property is leased, the lease amounts can be used so as long it's no more than 25% higher than market rents. For unleased purchases market rental rates will be used from the 1007 market rental survery done during the appraisal process. A DSCR ratio of over 1 means the property generates enough income to cover its debt obligations. Host Financial can finance deals with DSCRs .75 or below. 75 to .99, 1.00+, 1.25+ and above. In the rate calculation DSCR ratio plays a factor so for the best rates not withstanding of other qualifying factors (FICO, loan size, property type, LTV, etc), a DSCR ratio of 1.25 above would be considered a top tier bracket for rates.

-

Host Financial provides financing for various properties suitable for short-term rentals, including single family residences, condos, townhomes, duplexes, triplexes, quadplexes, and multi-family properties up to 20 units.

-

Host Financial typically requires a minimum credit score of 620 for short-term rental financing. However, for the best LTV, rate, and term options a credit score of 680+ is preferred.

-

The approval process at Host Financial involves submitting a request for a quote, selecting the loan term and option to move forward with, proceeding with an application, providing documents for under writing such as entity docs (if vesting under an entity), driver's license, 2 months bank statements for liquidity verification, insurance policy quote, title report, and payment for appraisal inspection. Once borrower files, insurance policy, title reports, and appraisal report is submitted the loan will go into final underwriting and qualify control. Once approved, we prioritize a swift and efficient closing process that takes five to ten business days.

-

Host Financial offers flexible loan terms tailored to the unique needs of short-term rental investors. Choose from 30 and 40 year amortization options with 5/6arm, 7/6 arm, 10/6 arm, 10 year IO, and 30 year fixed options.

-

Yes, a down payment is required. The amount may vary based on factors such as credit score, property type, and loan amount. Host Financials' team collaborates with you to determine the most favorable terms for your specific situation. Typical down payments range from 15 to 25% down.

-

No, once Host Financial finances the property, you have the freedom to use it for rentals as planned.

-

Absolutely. Host Financial takes into account projected market rents when quoting and offering preapproval letters. The final number used for underwriting will be confirmed via the appraisal 1007 market rental survey report.

-

Host Financial offers short-term rental financing with prepayment penalties ranging from 1 year to 5 years. Structures include option from a 5% or 3% flat prepayment penalty each year for the lenght of the pre-payment period term or a declining structure such as a 5/4/3/2/1, 5/4/2, 3/21, 3/0/0 (examples, not all inclusive).

-

Host Financial is committed to a smooth and timely closing process. While timeframes may vary, we strive to close long-term rental loans efficiently, typically within 25 days. The main timeframe hurdles for closing a loan that are outside of the borrowers control is the turnaround time on appraisal reports. In a cases in which insurance, title, appraisal report, and borrower side documents are turned in quickly closing can occur within one to two weeks from receipt of the complete list of files.

-

• One Stop Shop For DSCR Financing: In our current dynamic market environment, rates and even qualification guidelines change daily. Host has access to multiple capital partners and will price the entire market ensuring you get the best rates and terms available.

• Should rates changes mid process we can quickly switch capital partners to get a lower rate.

• Should guidelines change mid process you won’t be stuck with a lender that has one set of guidelines which could kill your deal and put you back to shopping the market. This ensures we have the highest chance of closing on deals where others can’t.

• Host Financial are the experts in DSCR financing: 95% of our deals are for DSCR loans for rental investment properties. Working with Host ensures you know you’re working with a lender that gets it and can get the deal done. We’ve seen and done it all.

• Privacy & Asset Protection: With the ability to vest in an entity you can protect your identity and assets from the risks and liability involved with running a long term rental property.

• Most coverage: Host lends in 48 states nationwide.

RENOVATION & NEW CONSTRUCTION LOAN FAQs

-

A Renovation or New Construction loan is a type of loan that includes additional funds as part of the loan to help renovate and/or build the property.

-

Unlike DSCR loans where the income of the property is the primary qualification factor, Renovation/New Construction loans are qualified primarily based on past project experience of the borrowers. The more experience the borrower(s) have in completing Renovation/New Construction projects, the more advantageous the loan terms.

-

Yes, it is possibly to qualify for a Renovation or New Construction loan without any prior experience.

-

Renovation/Construction loan sizes are determined based on a Loan to Cost (LTC) vs Loan to Value (LTV) calculation. Generally the Renovation/New Construction Loan can fund up to 80% - 90% Loan to Cost (Purchase Price + Budget) so long as that loan amount does not exceed 70% - 75% of the completed value (LTV) of the project.

-

Generally 6 months to 18 months in duration, 8% - 12% rate and Interest Only payments with 1-3% origination fees, depending on the experience level of the borrower, FICO score, loan amount and other associated deal terms.

-

Generally no, there are no pre-payment penalties. As soon as the project is complete, the loan can be refinanced or paid off.

-

All typical residential property types are eligible – Single Family Homes, Townhomes, Condos, 2 – 4 Unit and 5 – 8 Unit Multi-Family properties. Financing for larger commercial projects such as 9+ Unit Multi-Family, Retail, Mixed-Use, or Office are also available on a case by case basis.

-

A licensed General Contractor is almost always required for a New Construction project. For a renovation project, it will largely depend on the scope of the renovation work, but a general contractor is not always required.

-

This will depend on the scope of the work being performed and the requirements of the local jurisdiction where the project is located.

-

Yes, the cost of the land is included in the total cost basis of the project and can be included in new construction loan.

-

Yes, rural properties are eligible. Generally, would like to see a proven track record on completing similar rural type properties.

Don’t see your question answered here?

We’re here to help. Fill out our contact form and we will get back to you with more information.

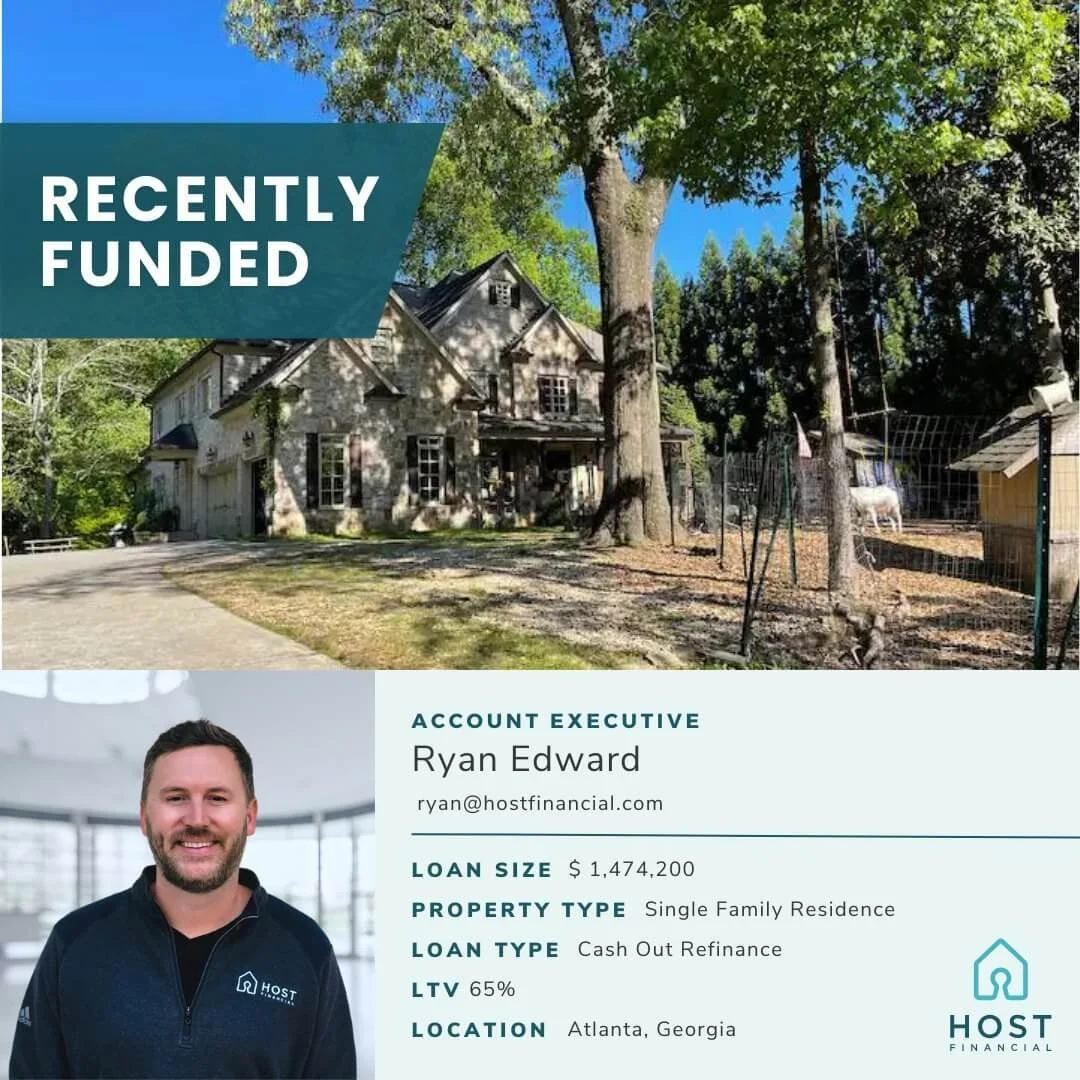

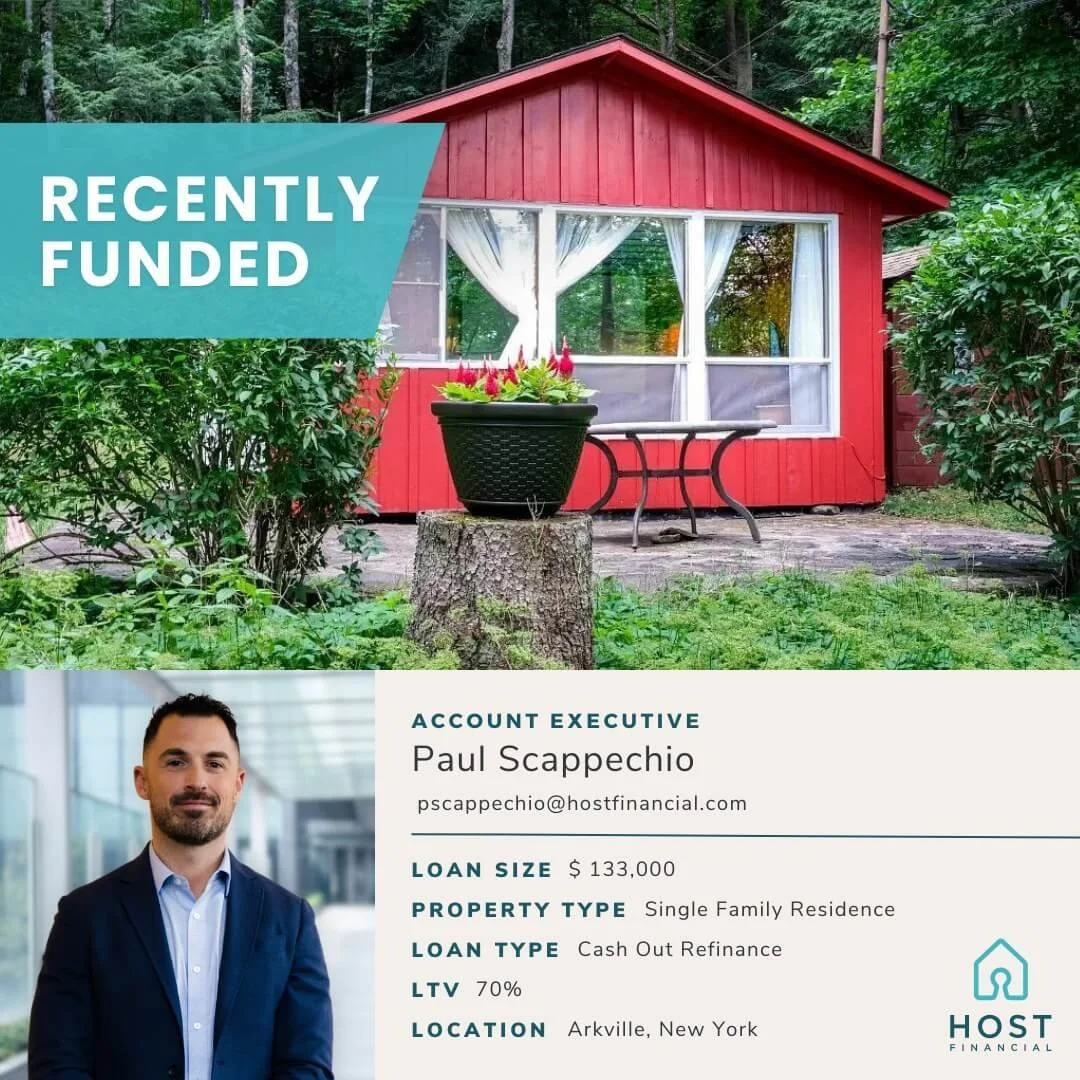

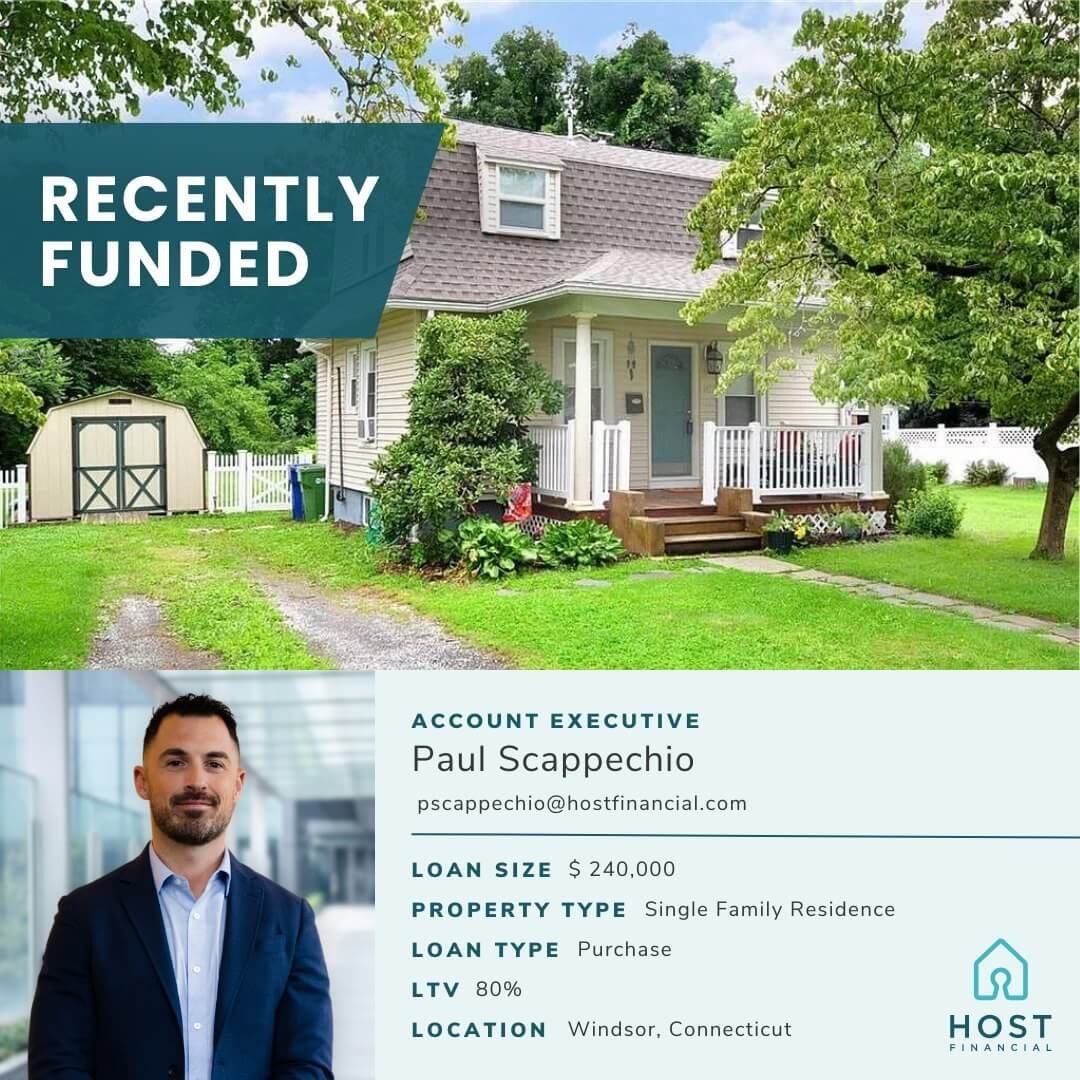

Recently Funded

Curious to know if you can apply to get financing for your investment property in your area?

Check out all the sates we service and see if you could qualify! Our lending partners lend across the county in 48 states.